(Especially for Indian Millennial and Gen Z Balancing Freedom vs Hustle)

Explore the FIRE movement in 2025 from an Indian perspective. Can millennial and Gen Z really retire early? Discover practical tips, top investment strategies, and actionable steps toward financial freedom.

🚀 Introduction: The Rise (and Reality) of the FIRE Dream

Imagine sipping coffee in the hills of Himachal at 40, free from the 9-to-5 grind. That’s the dream the FIRE Movement (Financial Independence, Retire Early) promises. But here’s the question everyone’s asking in 2025: Is FIRE still realistic in today’s economy?

With rising inflation, job market uncertainty, and an evolving investment landscape in India, Gen Z and millennial are re-evaluating. They are questioning whether FIRE is a fantasy or an achievable goal.

Let’s break it down—with clarity, optimism, and real talk.

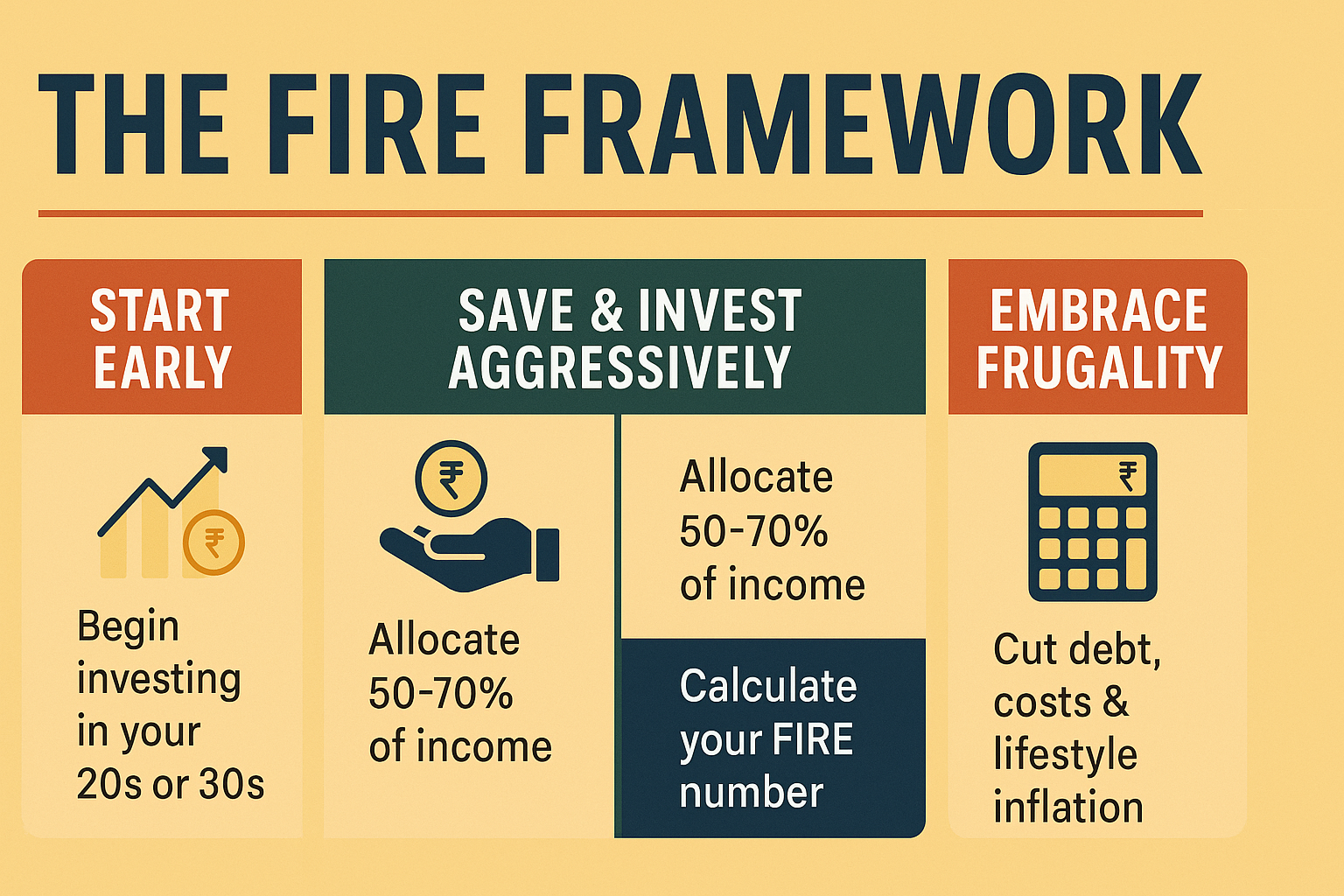

🔍 What Is FIRE—and Why Has It Captured India’s Young Minds?

FIRE isn’t about stopping work entirely—it's about gaining financial freedom to choose how you spend your time.

The movement is rooted in aggressive saving (50–70% of income) and smart investing. It is gaining traction among young professionals in India’s metros. This is especially true for those in tech, finance, and digital careers.

But the big shift in 2025? Many aren’t chasing full retirement at 35 anymore. They’re chasing “Work Optional” lifestyles.

🔗 FIRE number calculator by ClearTax India

👉 https://cleartax.in/s/fire-retirement-calculator

📈 Why Retirement Planning Is More Crucial Than Ever (Even If You Don't Want to Retire Early)

Let’s face it: pensions are gone, and EPFs won’t cut it. In India, with life expectancy rising and healthcare costs skyrocketing, retirement planning isn’t optional.

Whether you want to FIRE at 40 or just retire peacefully at 60, the key is early investment. It should be tax-efficient and diversified.

💼 Best Investment Strategies for Retirement in 2025 (From an Indian Lens)

🏦 1. Mutual Funds & SIPs: The Indian Favorite

Systematic Investment Plans (SIPs) in equity mutual funds offer compounding, tax efficiency (under ELSS), and flexibility. Ideal for salaried millennial.

🔑 Tip: Start with ₹5,000/month in a large-cap or index fund; increase annually by 10–15%.

📊 2. Direct Stocks: High Risk, High Reward

Indian retail investors are flocking to stocks. The FIRE crowd prefers long-term investing in fundamentally strong businesses. Examples include TCS, HDFC, or Infosys.

Avoid FOMO trading. Stick to value-driven portfolios.

🏘️ 3. Real Estate: Still Relevant?

Yes—especially in Tier-2 cities and for rental income. But high entry costs and low liquidity mean it should be part of your portfolio, not your whole plan.

🔎 REITs (Real Estate Investment Trusts) are a low-cost way to diversify into real estate with better liquidity.

💰 4. NPS, PPF & Tax-Saving Tools

- NPS (National Pension Scheme): Offers tax benefits under 80CCD and partial equity exposure

- PPF: Risk-free and tax-free but has a lock-in

- ELSS Mutual Funds: Combine tax-saving and equity growth

Smart FIRE followers use a mix of NPS + SIPs + REITs to build a tax-optimized core.

🧠 Proven FIRE-Friendly Strategies

🌱 Start Early, Even Small

Compound interest is your best friend. A 25-year-old investing ₹10,000/month can retire with over ₹3 Cr by 50 at modest returns.

🎯 Define Your “Enough”

FIRE isn’t about being rich—it’s about having enough. Calculate your monthly expenses × 300 to know your FIRE number.

Example: ₹50,000/month × 300 = ₹1.5 Cr needed to FIRE.

📉 Cut Lifestyle Inflation

Resist the "salary = spending" trap. Use income hikes to boost investments, not EMI burdens.

🧾 Track & Automate

Use apps like INDmoney, ET Money, or Groww to track net worth and auto-invest.

😬 Common Mistakes FIRE Aspirants in India Should Avoid

- 📉 Underestimating healthcare costs (get health insurance early)

- 🛍️ Over-spending due to social pressure or FOMO

- 📉 Not planning for inflation (target 10–12% returns long term)

- 📅 Ignoring rebalancing or being too aggressive late in career

💡 Actionable 5-Step FIRE Plan for Indian Millennial & Gen Z

- Evaluate Your Finances: Debt, expenses, savings

- Set FIRE Goal: Age, lifestyle, number (FIRE Calculator helps!)

- Invest Smartly: SIPs, NPS, ELSS, stocks, gold, REITs

- Review Quarterly: Unbalance and update goals

- Stay Frugal Yet Fulfilled: FIRE is about freedom, not deprivation

🧾 Real-Life Example: Could You Be Like Priya, Age 34?

Priya, a Bengaluru-based IT professional, started investing ₹15,000/month at age 25 in mutual funds and NPS. She avoided car loans. She lived in a rented apartment. She freelanced on weekends. By 2025, she has ₹85L corpus with side hustle income of ₹40K/month.

She’s not “retired”—but she doesn’t need to fear layoffs anymore. That’s true freedom.

❓FAQs on FIRE & Retirement Investment in India

Q: Can I FIRE in India making ₹12 LPA?

Yes—if you save aggressively (50%+), avoid debt, and invest smartly.

Q: Which are the best stocks for retirement savings?

Index funds (Nifty 50), dividend-paying blue chips like ITC, Infosys, or HDFC Bank.

Q: Is it safe to rely only on SIPs?

Diversify across SIPs, PPF, NPS, and even digital gold or REITs.

Q: What if I start late, say at 35?

You’ll need to invest more per month or push retirement age—but FIRE is still possible.

🔚 Final Thoughts: Is FIRE Dead or Just Growing Up?

FIRE in 2025 isn't about quitting at 35 and moving to Goa. It's about buying freedom, peace of mind, and choices. In India, the rising gig economy, remote work culture, and digital investing tools make FIRE more accessible. Still, this is only true for those who plan smart.

Whether you dream of retiring early or just want to escape paycheck anxiety, the principles of FIRE are key. These principles include frugality, investing, and intentional living. They will always stay relevant.

🥡Takeaway:

Start small. Stay consistent. Design your own definition of freedom. FIRE isn’t just possible—it’s personal.

🔗 References for FIRE & Retirement

- Reserve Bank of India – Handbook of Statistics on Indian Economy

It provides reliable macroeconomic indicators. Additionally, it shows long-term inflation trends useful for planning future retirement needs.

👉 https://www.rbi.org.in/Scripts/AnnualPublications.aspx?head=Handbook%20of%20Statistics%20on%20Indian%20Economy - NPS Trust (National Pension System Official Portal)

Ideal for referencing government-backed retirement tools with tax benefits (80CCD).

👉 https://www.npstrust.org.in - AMFI India (Association of Mutual Funds in India)

Offers beginner-friendly guides on SIPs, mutual fund selection, ELSS, and tax-saving funds.

👉 https://www.amfiindia.com - ET Wealth (The Economic Times - Personal Finance Section)

Trusted for expert-backed financial planning articles. It includes features on the FIRE movement. There are also comparisons of retirement strategies.

👉 https://economictimes.indiatimes.com/wealth - SEBI Investor Education – Mutual Fund and Retirement Planning Guides

This is great for linking educational content around safe investing. It helps avoid retirement planning mistakes.

👉 https://investor.sebi.gov.in